The global payments landscape is at an inflection point. Over the past decade, domestic systems such as Brazil’s Pix, India’s UPI, and Kenya’s M-Pesa have redefined what is possible within national borders: instant settlement, near-zero fees, and broad financial inclusion.

Platforms that enable fast, reliable, and low-cost payments are no longer aspirational. They operate at scale. Those systems are siloed by design, however. Each maintains its own standards for identification, compliance, and settlement.

Crossing borders normally requires reverting to legacy correspondent banking, with all the familiar frictions of foreign exchange spreads, delays, and intermediaries. The paradox is clear: within borders, payments are faster and cheaper than ever. Across borders, payments remain slow, costly, and operationally complex.

The next generation of payments will not be built by replacing these national networks. It will be built by connecting them, with stablecoins acting as the neutral, programmable settlement layer.

Local Rails Are Fast and Cheap, but Fragmented

The first generation of digital payment infrastructure has already reshaped national economies. Experimentation toward faster payments has become a pillar of global financial infrastructure, embedded in daily commerce.

Domestic Networks as Critical Infrastructure

In Brazil, Pix has become ubiquitous, with near-instant settlement and universal reach across consumers and businesses. By Q2 2024, Pix processed more than 15.4 billion quarterly transactions, making it one of the largest real-time payment systems in the world.

India’s Unified Payments Interface (UPI) scaled even further. The platform now consistently clears 15–20 billion monthly transactions, powering activity from small-scale merchants to multinational corporations.

In Kenya, M-Pesa has transformed financial inclusion, lifting millions into the formal economy by making payments and savings available via mobile phone. A World Bank study found that by 2009, average M-Pesa users were twice as likely to have a bank account as compared to non-users.

Why Interconnection Remains Out of Reach

These systems prove a critical point: domestic rails can be both efficient and cheap. They show that governments and central banks can build modern payment architecture and deliver broad adoption. Real-time settlement and meaningful cost reductions are among the clear benefits provided.

In many respects, these systems have leapfrogged legacy banking rails that remain burdened by batch processing and limited availability.

However, their very success underscores the limitations.

The World Bank estimates that global remittance costs still average 6.49%; a stark contrast to the near-zero fees on domestic transfers through Pix or UPI. Intermediary layers, FX exposure, and settlement delays continue to weigh on the movement of money across borders.

Stablecoins and Blockchain as a Neutral Settlement Layer

Domestic payment rails are effective within their own borders, but they fail to solve the shortcomings of global payment systems, most notably, a lack of interoperability. That role is increasingly being filled by stablecoins and blockchain infrastructure, which together create a neutral layer capable of connecting fragmented national rails.

Programmable Infrastructure for Global Settlement

Stablecoins represent traditional money in tokenized form. They’re redeemable on demand and sent across open networks, like Ethereum, Polygon, and Solana. When issued under credible frameworks, stablecoins combine both the stability of government-issued money with the benefits of digital assets.

Blockchains, in turn, provide neutral options for settlement. They are becoming a core financial infrastructure that no single government or bank controls. The demand for decentralized dollars has been validated by the explosive growth of on-chain tokenized assets. RWA.xyz shows that outstanding supply for on-chain U.S. Treasuries surpassed $3.6 billion by mid-2025.

Compliance requirements (e.g. KYC, AML, KYB, etc.), conditionality, and risk management can be embedded directly into payment workflows, enabling broader use cases, such as payroll, treasury management, and institutional asset management via stablecoins.

For institutions, this enables automated reconciliations, transparent audit trails, and real-time enforcement of regulatory obligations. For end-users, it translates to lower costs and fewer intermediaries without sacrificing trust.

Beyond speed and cost, programmability will blur the line between settlement and logic. Payments will become conditionally executed, triggered by smart contract parametrers. A corporate payroll, for example, could execute automatically once on-chain performance data confirms that work has been completed.

Why Stablecoins Are Better Positioned Than Bitcoin/Lightning

The Bitcoin Lightning Network has demonstrated valuable concepts, including liquidity routing, atomic multipath payments, and the resilience of open rails. But Lightning remains niche, with limited liquidity depth and little regulatory clarity.

Stablecoins, by contrast, are already embedded in institutional workflows. They have benefited from regulatory progress, including the GENIUS Act in the United States, MiCA in Europe, and a growing set of frameworks across other jurisdictions. Market adoption is equally decisive: stablecoins represent hundreds of billions in circulating supply, with daily transaction volumes to rival traditional payment networks.

This positioning makes stablecoins a more practical foundation for interconnection. They combine the trust of fiat backing with the openness of public blockchain settlement, while being deployable in contexts where compliance and auditability are non-negotiable.

Together, stablecoins, blockchain, and high-speed local rails form the first neutral foundation for global settlement that any institution can build upon. Infrastructure and operational layers can translate neutrality into an open channel where money can move with the same speed and certainty as information, across borders.

The Building Blocks of an Interconnected Network

Stablecoins and blockchain provide a clear channel for transactions, but delivering a usable global payments fabric requires operations to become intertwined with issuance.

This is the defining period: where high-speed national payment systems like Pix, UPI, and M-Pesa plug into global settlement without changing their core design. To make that work, Institutions need operational layers that abstract away complexity andensure reliability, while also including compliance by default.

Four components stand out as critical to realizing this model.

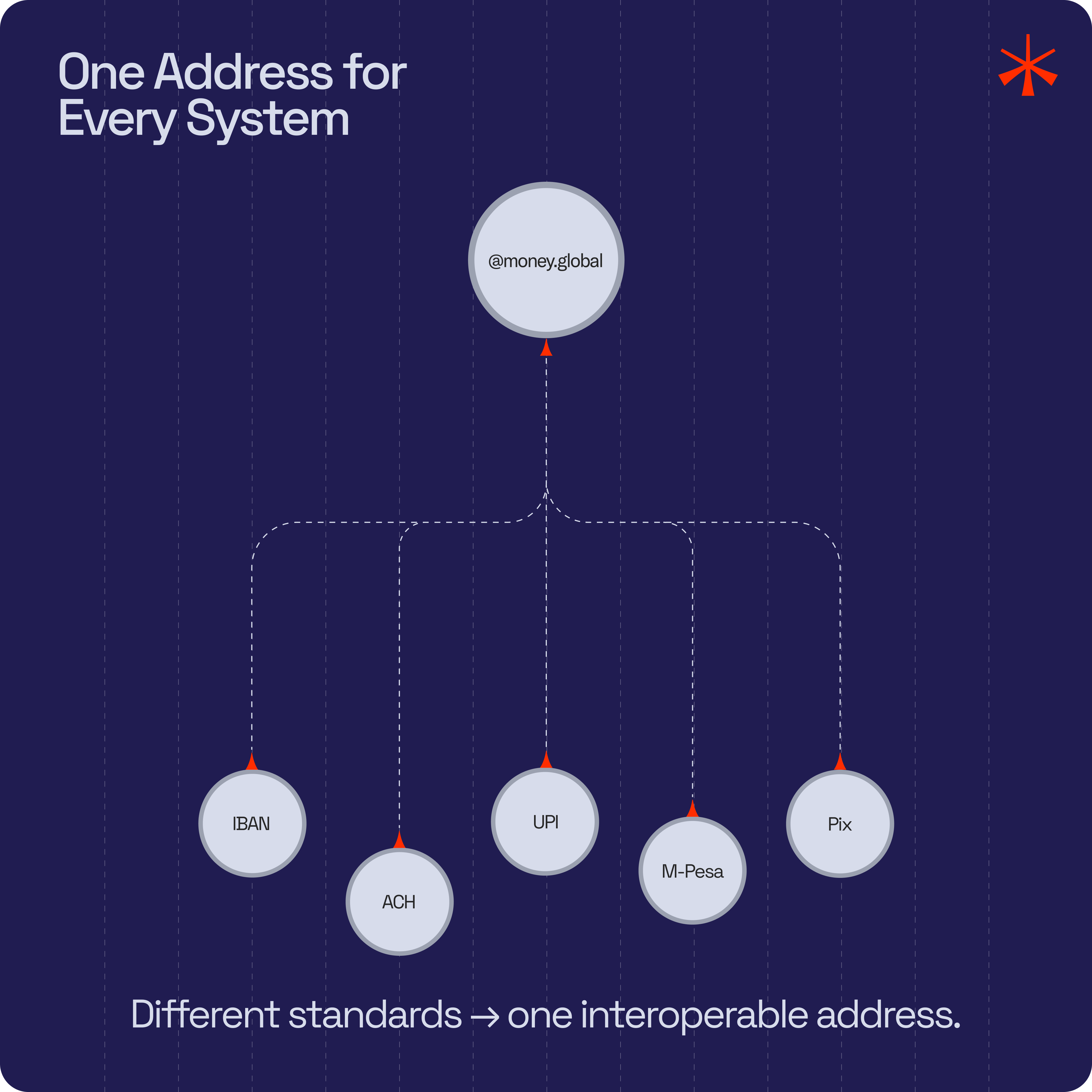

Universal Addressing Layers

The first challenge is identification. Today, domestic systems rely on their own standards; IBANs in Europe, bank account numbers in the United States, and mobile numbers in Kenya. This fragmentation creates friction for cross-border payments, where senders must understand the format and requirements of each destination.

Virtual addressing abstracts away these differences. One address can be mapped to multiple identifiers, enabling a user in India to send funds from a UPI-linked account to a Pix-linked wallet in Brazil without handling the underlying details.

For enterprises, it reduces integration costs; for consumers, it makes payments feel as seamless as sending an email.

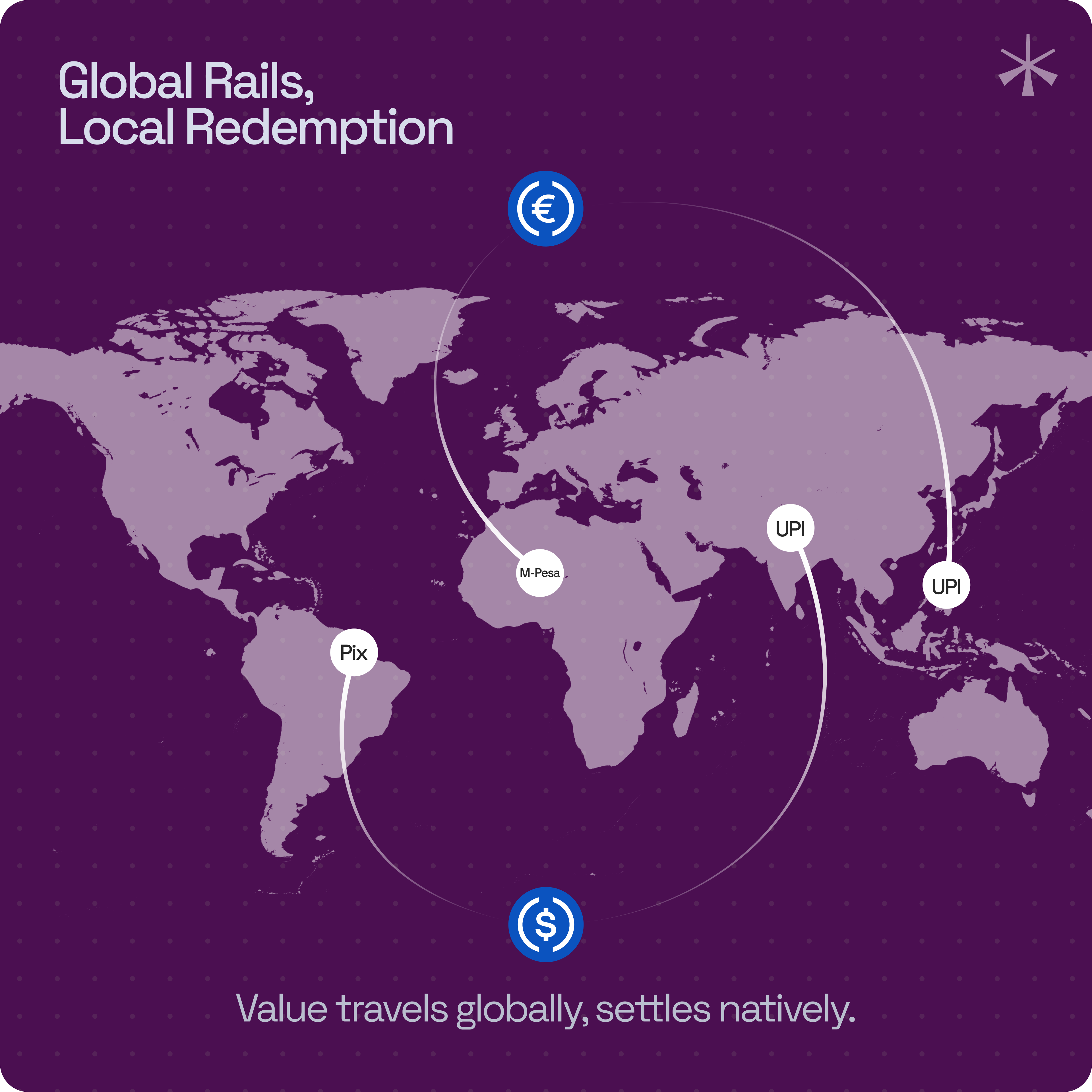

Stablecoins That Settle Locally

Global interoperability must not come at the expense of local usability. Stablecoins pegged to domestic currencies or instantly redeemable into domestic rails will allow value to arrive in-country without introducing FX exposure.

This approach protects end-users who need to spend in local currency, while preserving national monetary sovereignty. It also ensures liquidity is available where it matters most: at the last mile of the transaction. Fusing stablecoin rails with local settlement systems will cause cross-border payments to feel identical to domestic transfers.

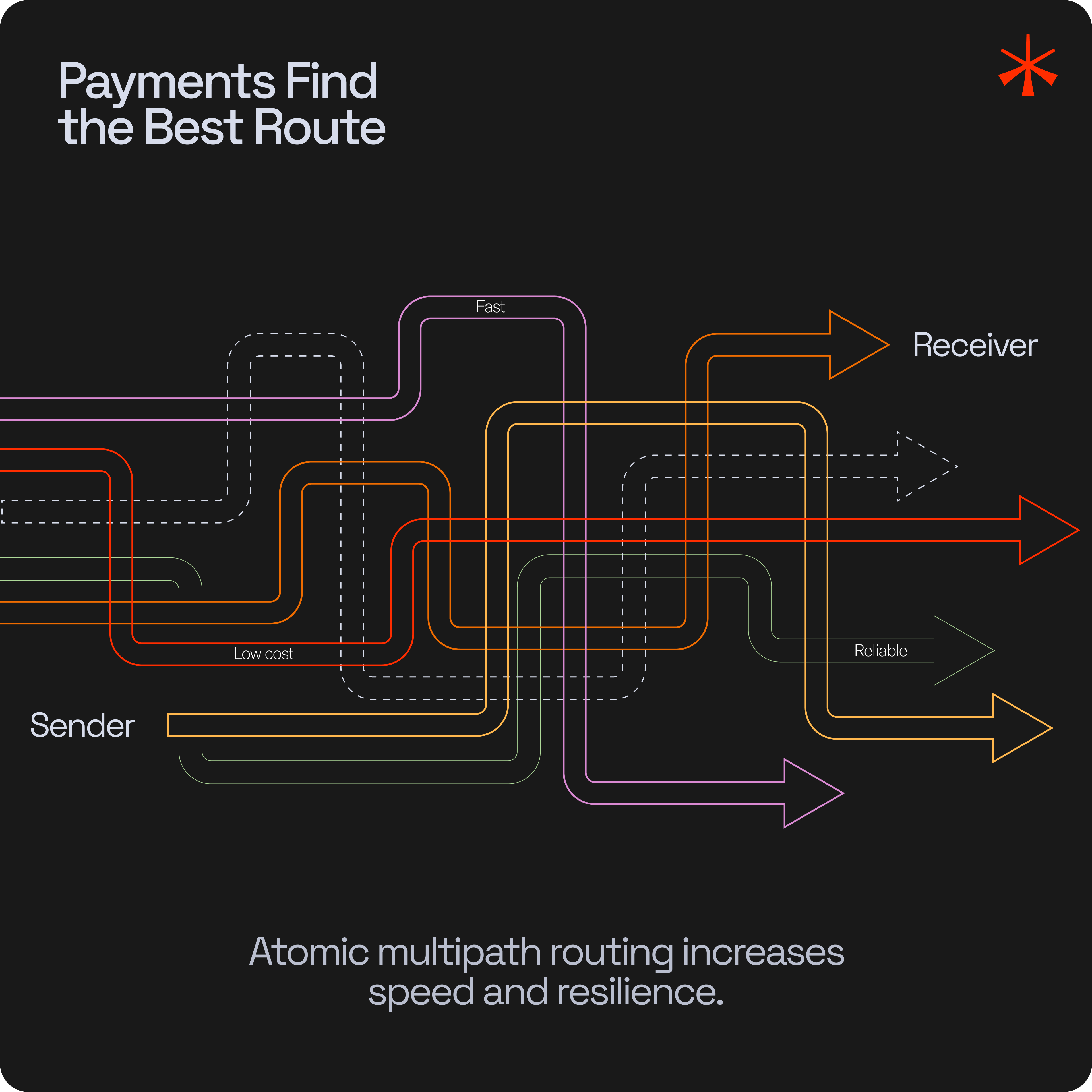

Dynamic Liquidity Routing and Multi-Path Payments

Interoperability is meaningless if payments fail in practice. Around 90% of SWIFT payments succeed within 24 hours, but some must be retried. Cross-border transactions face liquidity constraints, fragile intermediaries, and path inefficiencies. Without robust routing, settlement speed and cost advantages evaporate.

Here, lessons from the Lightning Network apply.

Atomic multipath payments and dynamic routing engines distribute transactions across multiple liquidity paths, increasing success rates and optimizing costs. Enterprise providers are already adapting these tools to stablecoin flows, ensuring that liquidity bottlenecks do not undermine the reliability of global payments. For institutions managing large volumes, routing resilience is a prerequisite for adoption.

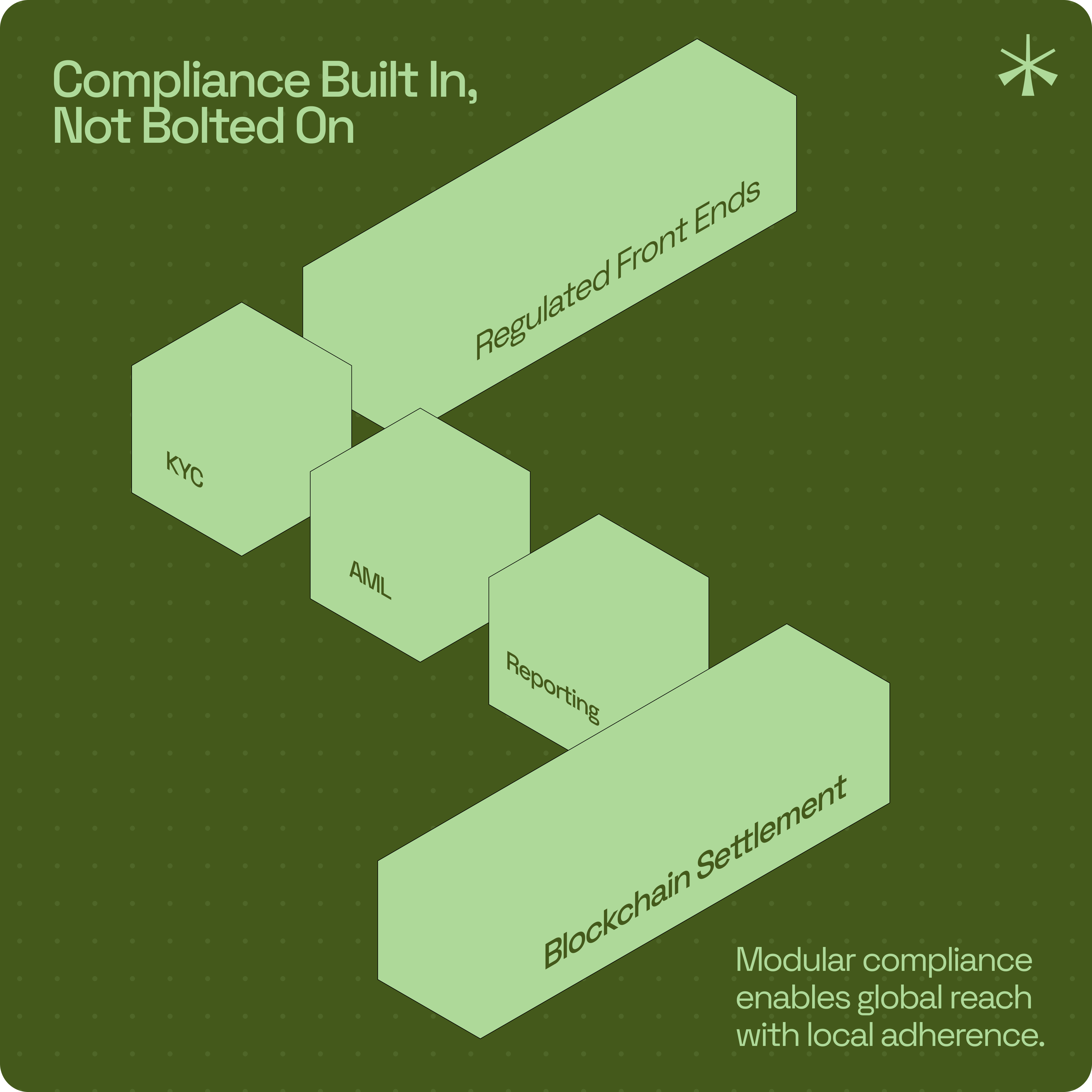

Compliance as a Modular Layer

Finally, the system must operate within regulatory boundaries. Payments infrastructure cannot scale globally if compliance is bolted on as an afterthought. At the same time, embedding rules directly into blockchain protocols risks inflexibility or jurisdiction-specificity that could compromise the interoperability benefits of the novel infrastructure.

The solution is modular compliance. Regulated front-end providers handle KYC, AML, and reporting, while settlement layers remain neutral. This separation enables consistent local adherence without fragmenting the underlying network. For institutions, it offers confidence: they can transact globally on open infrastructure while remaining fully compliant in each jurisdiction.

Dynamic Liquidity Routing and Multi-Path Payments

Interoperability is meaningless if payments fail in practice. Around 90% of SWIFT payments succeed within 24 hours, but some must be retried. Cross-border transactions face liquidity constraints, fragile intermediaries, and path inefficiencies. Without robust routing, settlement speed and cost advantages evaporate.

Here, lessons from the Lightning Network apply.

Atomic multipath payments and dynamic routing engines distribute transactions across multiple liquidity paths, increasing success rates and optimizing costs. Enterprise providers are already adapting these tools to stablecoin flows, ensuring that liquidity bottlenecks do not undermine the reliability of global payments. For institutions managing large volumes, routing resilience is a prerequisite for adoption.

Compliance as a Modular Layer

Finally, the system must operate within regulatory boundaries. Payments infrastructure cannot scale globally if compliance is bolted on as an afterthought. At the same time, embedding rules directly into blockchain protocols risks inflexibility or jurisdiction-specificity that could compromise the interoperability benefits of the novel infrastructure.

The solution is modular compliance. Regulated front-end providers handle KYC, AML, and reporting, while settlement layers remain neutral. This separation enables consistent local adherence without fragmenting the underlying network. For institutions, it offers confidence: they can transact globally on open infrastructure while remaining fully compliant in each jurisdiction.

Real-World Use Cases

The value of an interconnected payments fabric is most evident when applied to real-world transactions. Remittances, wallets, and embedded finance providers are poised to benefit most immediately from a system that fuses domestic rails with stablecoin settlement.

Remittances at Lower Cost and Higher Speed

Global remittances total more than $860 billion annually, a lifeline for families across LATAM, Africa, and Southeast Asia. Yet costs remain persistently high, averaging 6.49% per transaction according to the World Bank. For a worker sending $200 home, that is $13 paid to intermediaries, multiple days of food for a family in Brazil.

Interconnecting local rails through stablecoin settlement can reduce these costs to a fraction of one percent. Funds move on open blockchain rails and settle directly into domestic systems like Pix or UPI. The results include: faster delivery, higher net income for recipients, and greater financial stability for households.

Wallets, Neobanks, and Embedded Finance Providers

For fintechs, the challenge is achieving global reach without stitching together dozens of bilateral integrations. Wallet providers and neobanks can integrate once into a stablecoin settlement layer, instantly gaining access to multiple domestic rails.

In Africa, for example, over 82% of all cashless payments were transacted using Nigeria’s NIP system. In LatAM, ~70% of all fintechs specialize in lending, payment acceptance, and wealth management. It’s clear that business function is the highest priority among emerging businesses.

Real-world use cases highlight the structural advantages of interconnected networks. Faster, cheaper, and more inclusive flows that service households and enterprises alike.

The Cost of Trust: Why Open Systems Endure

Interconnecting payment systems requires durable trust in the underlying infrastructure. Closed networks can deliver speed and efficiency within their borders, but they rarely scale.

Limits of Closed Systems

Proprietary blockchains or walled-garden solutions replicate the limitations of domestic rails: interoperability is constrained by who controls access. By contrast, open systems proliferate because they’re neutral and impartial. Public blockchains provide a settlement channel that no single government or vendor can monopolize.

Neutrality is a structural necessity. Institutions rely on open rails precisely because they cannot be unilaterally shut down or constrained by a single jurisdiction’s policy shift. Stablecoins extend the model by combining open infrastructure with fiat-backed stability and regulatory alignment. The resulting settlement layer is both trusted and usable across jurisdictions.

The Strategic Value of Neutrality

The value of trust is significant. Building on closed networks risks vendor lock-in and exposes institutions to both counterparty and regulatory risk. Building on open rails shifts trust to the protocol layer, where transparency, auditability, and global participation are the building blocks of systemic resilience.

For the next generation of payments, this distinction will be a key determinant in longevity. The global payments fabric will rely on infrastructure that is neutral and composable because these systems can sustain institutional trust at scale.

The Bank for International Settlements (BIS) Committee on Payments and Market Infrastructures (CPMI) has emphasized that “interlinking fast payment systems is the most efficient path to cross-border integration.”

Strategic Implications for Institutions

The opportunity in next-generation payments will not come from rebuilding domestic systems. Local rails such as Pix, UPI, and M-Pesa are entrenched and politically reinforced. The strategic opening is rooted in interconnect the fragments; delivering a viable connection that links national systems into a grander, global fabric.

From “Owning the Stack” to “Owning the Connectivity”

For institutions, this requires a shift in mindset. The goal is no longer to “own the stack,” but to own the connectivity: universal addressing, compliant onboarding, reliable routing, and liquidity for the edges. The firms that provide these layers are abstracting away local complexity while ensuring regulatory alignment. They will become indispensable partners across the ecosystem.

The Payments Fabric of the Future

The benefits extend beyond payments. Interconnection reduces operational costs, opens new revenue corridors, and positions institutions to serve clients in markets that were previously uneconomical. From cross-border trade finance to embedded payouts for digital platforms, the addressable opportunity is global.

Crucially, this is not an incremental upgrade. It is a structural rewiring of how value moves. Institutions that invest early in compliance-ready, stablecoin-enabled connectivity will be positioned to define the next decade of payments, while those that wait risk being constrained by the very silos their clients seek to escape.

The future of payments will not be defined by tearing down domestic systems, but by interconnecting them. Domestic settlement rails, including UPI, SEPA Instant, and M-Pesa, have proven that they remain bounded by borders, unable to deliver seamless global settlement on their own.

Stablecoins and blockchain provide the missing connective tissue: a neutral, programmable settlement layer that bridges national champions into a global fabric. With universal addressing, local settlement, dynamic routing, and modular compliance, institutions can translate the promise of open rails into operational reality.

This is a structural rewiring of how value moves across the world; faster, cheaper, and more inclusive than the systems it overlays. The institutions that master interconnection will not simply participate in this shift; they will define the next decade of global finance.