In a landmark victory for the broader crypto industry, the U.S. Congress passed the GENIUS Act on July 17, 2025, granting payment stablecoins their first federal green light.

For the first time, stablecoins like USDC and PYUSD are recognized in law as fully-reserved, cash-equivalent instruments. Payment stablecoins are inextricably tethered to ≤ 93-day T-bills, but without a Federal Reserve backstop, unlocking new clarity and scale, as well as introducing novel pressure points for markets and treasurers to navigate.

After years of legal grey, the US now offers stablecoins a clear statutory lane. GENIUS efficiently does four things that market participants have spent half a decade lobbying for:

- Defines “payment stablecoins” in law so that stablecoins can be treated as cash equivalents rather than securities;

- Installs full-reserve standards that market participants already clearly understand (e.g. sub-93-day treasuries);

- Creates a single prudential regulator per-issuer; AND

- Signals that digital dollars are a strategic priority for US competitiveness

These wins will accelerate adoption. Fireblocks’ 2025 Corporate Adoption Survey shows that regulatory clarity slashes corporate hesitation by as much as 60%. A recent analysis by Standard Chartered Bank highlights the growth potential that may be unlocked through regulatory clarity, predicting a potential tenfold surge in the number of circulating stablecoins by the end of 2028.

Why we still need a playbook:

Clarity alone doesn’t de-risk interconnected markets. The GENIUS Act wires stablecoin reserves directly into a T-bill complex that the Treasury Borrowing Advisory Committee (TBAC) projects will grow to $1.7T in net issuance this fiscal year, with bills reaching 22% of outstanding debt.

Top-of-Book depth for 4-week bills, however, averages <$25 million and collapses by up to 70% on tax days and quarter ends. If a major stablecoin were to wobble on a thin liquidity day such as this, issuers and gateways could be forced to liquidate bills to fulfill their redemption and off-ramp obligations, ricocheting through money-market funds and repo desks before the Fed has time to react.

The brief below maps that thin-liquidity scenario across two case studies and lays out some controls that treasurers, processors, and exchanges can deploy so GENIUS becomes a growth catalyst, not a systemic stress amplifier.

The Strategic Upside of GENIUS

GENIUS marks a pivotal moment in the crypto industry and finance at large. Stablecoins are poised to update or replace dated payment rails that leave corporate treasuries and multi-local businesses exposed to slow settlement and FX swings. Our recent blog explores some reasons that businesses are switching to USDC, highlighting the value of regulatory clarity.

Regulatory Legitimacy Unlocks Scale

90% of respondents to Fireblocks’ 2025 survey further affirm that regulatory and industry standards are driving adoption. GENIUS cements that momentum: it hard-codes “payment stablecoins” into federal law, giving finance teams the confidence to treat tokens as regulated cash-like instruments rather than experimental rails.

Treasury Efficiency Drives Incremental Bill Demand

The GENIUS Act requires every dollar of circulating stablecoin to sit in ≤ 93-day T-Bills, repos, or Fed balances. JPMorgan projects that, on this path, stablecoin issuers could rank as the world’s third-largest holder of short-dated Treasuries. The result is a self-reinforcing loop: deeper demand for safe collateral, 24/7 convertibility for corporates, and a stronger global dollar footprint.

What GENIUS Means For Processors and Exchanges

Exchanges that custody tokens through a qualified-trust structure can place issuer reserve cash and exchange treasury into ≤ 93-day T-Bills, then tap FICC-sponsored repo lines for same-day liquidity. This converts otherwise idle capital into a secured funding channel, without breaching GENIUS segregation requirements or relying on a Fed backstop.

Hosted-wallet PSPs must meet GENIUS Section 8’s full QC requirements:

- Full Segregation of Funds

- CPA Attestations

- Daily Reconciliation

- No Rehypothecation

Treasury teams, payment processors, and exchanges will now operate within a defined liability structure: only the stablecoin issuer can mint or redeem, and redemptions flow directly onto legacy balance sheets. These tokens function as 24/7-settling liabilities, backed by assets such as bank deposits, T-bills, and repos that settle on T+1.

Hidden Fault Lines That Demand Attention

“The GENIUS Act doesn’t eliminate risk. Instead, the new law results in stablecoin-related risks being more distributed to a variety of interconnected stakeholders, such as registered stablecoin issuers, public finance, and corporate treasuries, who are responsible for, and required to maintain effective controls to mitigate, a variety of new and emerging risks.”

—Emily Goodman, Partner, FS Vector

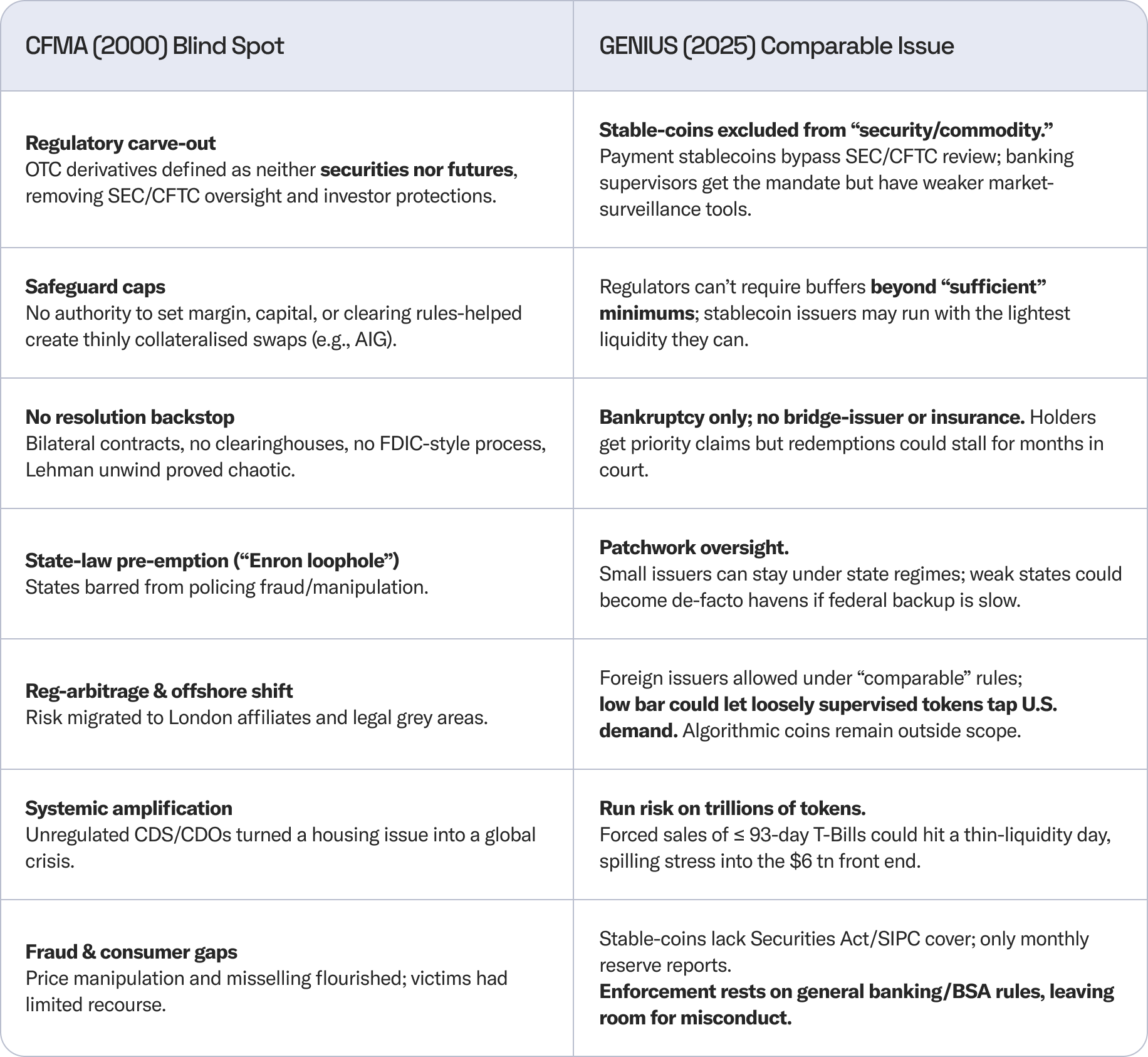

Oversight Carve-outs & Capital Constraints

Under GENIUS, payment stablecoins are exempt from Securities and Exchange Commission (SEC) and Commodity Futures Trading Commission (CFTC) regulation and enforcement. This lack of scrutiny, many argue, was a key catalyst in propelling the 2008 financial crash.

Some may argue that a similar regulatory oversight structure was in place and served as a key catalyst in propelling the 2008 financial crash

Further compounding the comparison between the Commodity Futures Modernization Act (CFMA) of 2000 and the GENIUS Act of 2025, regulators are inhibited from enforcing prudential liquidity buffer requirements on stablecoin issuers.

Contagion Paths: Run Risk & Treasury Shockwaves

Even outside a crisis, the Treasury market can hit calendar potholes when depth vanishes. Carrying specifically short-dated treasuries and MMFs alone, stablecoin issuers introduce a potentially unhedged point of failure into the treasury market, which forms the bedrock of global trade liquidity.

“Furthermore, because stablecoins will be increasingly embedded in mainstream balance sheets, certain risks tied to those assets, such as redemption and liquidity risk, may be shifted into traditional finance.”

—Emily Goodman, Partner, FS Vector

Thin-Liquidity Case Studies

Two recent “quiet-day” shocks prove that a sudden stablecoin unwind can move markets far beyond its footprint, especially with GENIUS offering no explicit lender-of-last-resort backstop, unlike the Fed’s safety net for banks and repo dealers.

Quarterly corporate-tax withdrawals and a heavy Treasury bill settlement drained dealer balance sheets; overnight GC-repo printed as high as 10% and the Secured Overnight Financing Rate (SOFR) jumped 282 basis points in a single session.

This non-crisis moment comprised the sharpest single-day increase ever recorded for the benchmark since the Fed’s repo-rate series began in 2001, with a prior record of +52 bp in Oct 2008, far larger than the ≤20 bp moves normally seen around quarter-ends. The Fed had to inject emergency liquidity within hours.

On a post-holiday Wednesday, the 10-year yield swung 37 bp intraday in just 12 minutes while order-book depth collapsed by up to 80%.

Stablecoin issuers will soon sit on a T-bill mountain. A confidence shock could force them to dump those bills precisely when Treasury depth is already "fragile," as regulators put it.

In March 2020, one prime MMF slipped under the 30% liquidity line (Rule 2a-7) yet chose not to gate redemptions. The SEC has since scrapped the gate option altogether, leaving only swing-pricing fees. If MMF outflows meet a token run, T-bill supply has nowhere to go but the screen.

The Institutional Playbook: Looking Forward

As stablecoins transition from niche crypto assets to core working capital rails, treasury teams need a playbook that treats them with the same levels of rigor and risk management as commercial paper, FX lines, or repo collateral.

The checklist below pairs immediate controls for today’s balance-sheet exposure with long-horizon levers to shape the rulebook itself. To help ensure that you’re not just reacting to tail events but helping hard-wire resilience into the market infrastructure you’ll rely on tomorrow.

“To prevent a stablecoin-led redemption run from becoming a T-bill fire sale scenario during a confidence shock, stablecoin issuers and infrastructure stakeholders must implement a variety of safeguards and risk mitigants, including those related to operational readiness, financial buffers, ledgering, transparency, and redemption discipline. These are some of the key components of the governance, enterprise risk management, and infrastructure maturation that will be required under the GENIUS Act.”

—Emily Goodman, Partner, FS Vector

Immediate Risk-Monitoring Actions

- Live reserve telemetry Subscribe to each issuer's on-chain proof-of-reserves feed (or the monthly CPA attestation where on-chain isn't available). Pipe the data into your treasury dashboard and flag deviations >10 bp from the target 1:1 ratio.

- Quarterly redemption drills Run a controlled $5 m–$25 m pull-through with every token you hold. Measure end-to-end settlement time, wire-receipt lag, and any fees. Document gaps for your liquidity playbook.

- Counterparty spread monitor Track the bid-ask and USDC/USDT basis on your core exchanges; a three-day widening >30 bp is an early stress signal. Couple it with CDS levels (where available) on the issuer's bank or trust parent.

- Diversified custody lanes Use at least two independent venues (e.g., self-custody + qualified custodian) and pre-approve an OTC desk for off-exchange exits.

- Pre-funded credit backstop Keep an evergreen draw-down line sized to one week of operating cash. If a liquidity crunch or MMF redemption fee strikes, you convert stress liquidity into orderly redemptions, not a fire sale.

Long-Term Engagement & Policy Advocacy

- Push for real-time attestations Support industry proposals that move from 30-day CPA snapshots to daily, or block-by-block, proof-of-reserves. Continuous transparency compresses run risk.

- Champion a swift-resolution regime Back trade association comment letters urging Congress to pair GENIUS with FDIC-style receivership and bridge-issuer authority. The goal: redemption continuity within 48 hours, not multi-month bankruptcy.

- Audit-threshold recalibration Advocate lowering the mandatory PCAOB-level audit bar from $10b to $1b in circulation; smaller issuers should not fly under the radar.

- Capital and liquidity buffers Support prudential add-ons (e.g., a 2% retained-earnings layer or mandatory access to the Fed's Standing Repo Facility) to absorb intraday shocks without dumping bills.

- Join the standards stack Participate in ISO 20022 stable-value extensions, the GFMA Digital Asset working group, and any Fed-orchestrated pilot on wholesale-token interoperability. Early involvement shapes playbooks you'll later have to live with.

Operational Liquidity Resilience for Processors and Exchanges

Stablecoin-based payment processors (PSP) and exchanges sit on the redemption frontline. In the event of lost confidence, users seek liquidity as quickly as they can (usually through the paths they already trust), which means exchanges and PSPs receive the first flow of off-ramp requests.

Exchanges have the opportunity to monetize GENIUS by offering white-label repo lines to Qualified Custodians. Traders can also pledge funds for overnight dollars, providing additional market depth and securing the market against demand shocks, within the provisions included in GENIUS.

Market Integrity and Compliance Considerations

Historically, regulators have leaned on gateways for enforcement of rules, including Circle and major node providers freezing funds after an OFAC/U.S. Treasury sanction of Tornado Cash in 2022. That obligation can be a competitive edge.

In the absence of an FDIC-style bridge issuer (not provided under GENIUS), exchanges must design their own continuity plans. Smart contract upgrade paths may be considered, allowing courts access to stuck payment stablecoins, similar to the bankruptcy-remote design currently used by mainstream custodians.

By hard-coding full-reserve payment tokens into U.S. law, Congress also hard-codes a direct link between stablecoin balance sheets and the Treasury front-end. A confidence shock could, therefore, ricochet from a token price wobble to a T-bill fire sale, straight into wholesale funding.

Contact us at business@noah.com or book a demo

Updated Risk Matrix