It’s 3:02 AM, and your company’s AI procurement agent identifies a favorable shift in supply chain pricing, negotiates a new contract, and settles a cross-border payment using stablecoins, settled in local fiat currency.

You save $65,000 while you sleep.

AI learned to form words in its infancy; now it’s learning to structure business agreements and manage payments reliably. To scale this autonomous economy, the foundational infrastructure is being built across two distinct layers: on-chain agentic transacting, and real-world fiat settlement.

McKinsey projects that agentic commerce will expand rapidly, orchestrating between $3 trillion and $5 trillion by 2030.

What Exactly are Agentic Payments?

Agentic payments are financial transactions that execute autonomously. The present landscape is defined with three tiers of autonomy:

- Agent-assisted payments

- Agent-directed payments

- Fully-autonomous payments

Where traditional payment system automation relied on rigid, rule-based logic, like monthly subscriptions and pre-programmed command execution, they held no capacity for dynamic reasoning, negotiation, or independent decision-making. Think of it like giving a corporate card to a long-tenured, trusted employee to negotiate supplier deals.

To safely execute an autonomous transaction, an AI must navigate six distinct capabilities:

- Knowledge (understanding the intent),

- Intelligence (finding the vendor),

- Trust (verifying the vendor),

- Authority (operating within constrained authorization),

- Settlement (executing the payment), and

- Accountability (providing cryptographic proof).

While conversational Large Language Models (LLMs) easily handle the knowledge and intelligence phases, the actual financial execution requires deterministic, cryptographically verifiable infrastructure. Agentic payments are not merely a user experience upgrade; to be safe for enterprise use, agent-initiated transactions must resolve to approved quotes, templates, and signed policies rather than free-form chat prompts.

Agent-assisted Payments

In Agent-assisted payments, the human remains the primary decision-maker.

A person is aware of their desire, so they ask an AI agent to assist them in sourcing items, comparing prices, and completing purchases. The person drives the transaction with their desire, awareness, and intent. An agent assists the buyer and completes the transaction.

For example, a consumer might ask an AI shopping assistant to find the best price on a laptop, source deals, apply coupon codes, and prepare the checkout screen, ultimately finding their dream machine at the best available price.

The autonomous assistant reduces friction, but the human still outlines the purchase conditions and completes the final payment authorization manually.

Agent-directed Payments

In agent-directed payments, a business establishes a set of parameters and then allows an agent to exercise operational discretion to accomplish a goal or set of goals. Humans hand over the reins for execution with agent-directed payments.

Users don’t manage every step in the process. Agents identify the opportunity, based on a preset mandate, for example, finding a supplier for a new business unit under a certain MOQ or rate per item. The agent will evaluate multiple options, decide on the best option based on the available information, and suggest the final authorization to the user.

Humans provide the overarching goal, budget, and risk parameters, leaving the operational implementation entirely to their digital counterparts.

Fully Autonomous Payments

In fully autonomous payments, agents identify each opportunity and close the loop on transactions at each step, without human intervention.

Fully autonomous should not be confused with uncontrolled. Autonomous systems are still built to operate within permissioned parameters. Someone still has to be accountable for the expenditure, long after it has been reconciled from the balance sheet.

For example, an AI agent can monitor supplier pricing across a number of sources, factor in discounts, bulk pricing, and negotiate new contracts, then settle the due balance, and reconcile the financials internally, all without human intervention.

Agentic transactions execute in milliseconds.

AI agents can process millions of sub-cent transactions with an API key.

They can operate 24/7/365.

They can function entirely without the AI needing a traditional bank identity.

Two Distinct Tracks of Agentic Commerce

To understand how this economy scales, enterprise leaders must separate the ecosystem into two distinct operational layers:

- Track 1: Agent-to-Agent Transacting (The On-Chain Economy): This track relies on specialized tools built for machines to transact with other machines natively. For example, Coinbase's x402 protocol embeds payments directly into basic web requests, meaning an AI does not need to "log in" or have an account to buy data. Circle's Nanopayments allow an AI to send fractions of a cent (like $0.000001) without paying massive network fees. Meanwhile, standards like ERC-8004 function as digital ID cards to prove an AI agent is legitimate, and Anthropic's Model Context protocol (MCP) helps agents discover what tools they can use.

Stablecoins win decisively where cards structurally fail. Processing sub-cent micropayments, executing 24/7 cross-border transfers, and providing permissionless access to global markets.

Consider the underlying economics: a standard credit card transaction costs 2% to 3% of the transaction value, as a variable fee alongside a flat baseline charge of around $0.30.

For an AI agent attempting to execute a $0.001 payment for a single second of compute power, a legacy payment rail with a $0.30 minimum flat fee can create costs upward of $1000/hr per agent.

Processing these sub-cent micropayments on traditional rails is mathematically unviable, whereas the near-zero cost of stablecoin infrastructure makes them not just viable, but sustainable.

- Track 2: The Aggregation and Exit Boundary (Real-World Settlement): Agents can transact freely on-chain, but eventually, accumulated value must enter the real economy. For example, an agent swarm might execute 10,000 sub-cent micropayments in Track 1. But at the end of the day, that aggregated $250,000 in USDC must be converted to Euros and deposited into a supplier’s traditional bank account. This exit boundary requires a fundamentally different architecture.

The Trust Gap: A Critical, Unsolved Problem

Despite this infrastructure, the industry faces an unsolved problem: the trust gap. The current bottleneck is that AI agents essentially operate with binary access: they either own full API key authority (essentially a blank check) or they have no spendable permissions.

A lack of delegated, constrained, and instantly revocable permissions operating at scale is preventing systems from maturing. Solving this requires four critical elements: delegated authority, policy as code, verifiable counterparties, and atomic settlements with receipts. The industry's emerging answer to this is the “Verifiable Intent” specification.

Think of Verifiable Intent as a programmatically-enforced corporate expense policy. Controls may be hard-coded constraints, or controls outside the agent’s scope that ensure compliance.

Rather than relying on a fragile text prompt, asking an AI to "please stay under budget," this framework hard-codes strict constraints, potentially including maximum transaction limits, cumulative budget caps, or specific approved merchants directly into the AI's authorization.

The agent cannot execute a payment outside these bounds, ensuring that its commercial actions are policy-constrained to a human's explicitly stated rules.

Honest State of the Market: Real vs. Hype

While McKinsey projects that agentic commerce will orchestrate between $3 trillion and $5 trillion of global commerce by 2030, today, Circle's data shows the average agent transaction is just $0.31.

To navigate this space, enterprise leaders must separate the hype from the reality:

- The Bullish View: There are currently over 400,000 AI agents with purchasing power that have executed 140 million payments. The stablecoin market cap exceeds $314 billion, Y Combinator is offering startup funding in USDC, and Forrester predicts that roughly one-third of B2B payment workflows will use autonomous agents by the end of 2026.

- The Sober Reality: While agentic payment protocols like x402 are seeing massive growth - surging from just $28,000 a day in mid-March to roughly $800,000 a day now - the absolute volume is still in its infancy. Only 24% of consumers currently trust AI to make purchases on their behalf, and Bloomberg recently noted that these agentic payments "barely exist" today compared to the trillions moving on legacy rails.

However, much like AWS in the early days of cloud computing, the foundational infrastructure is locking in right now, well before the massive consumer demand arrives.

Use Cases by Maturity

The application of these payments is scaling in distinct phases based on maturity:

- Live Now: The most mature stablecoin use cases involve API micropayments via x402, AI fraud detection, and agent-initiated checkouts, such as ChatGPT's integration with Etsy .

- Growing: We are seeing rapid expansion in agent-to-agent commerce, which is forecasted as a $46 billion opportunity over three years. This is growing alongside agentic treasury management and B2B procurement .

- Emerging Frontier: The next massive wave includes cross-border stablecoin payouts, agent marketplace settlement, and machine-to-machine payments .

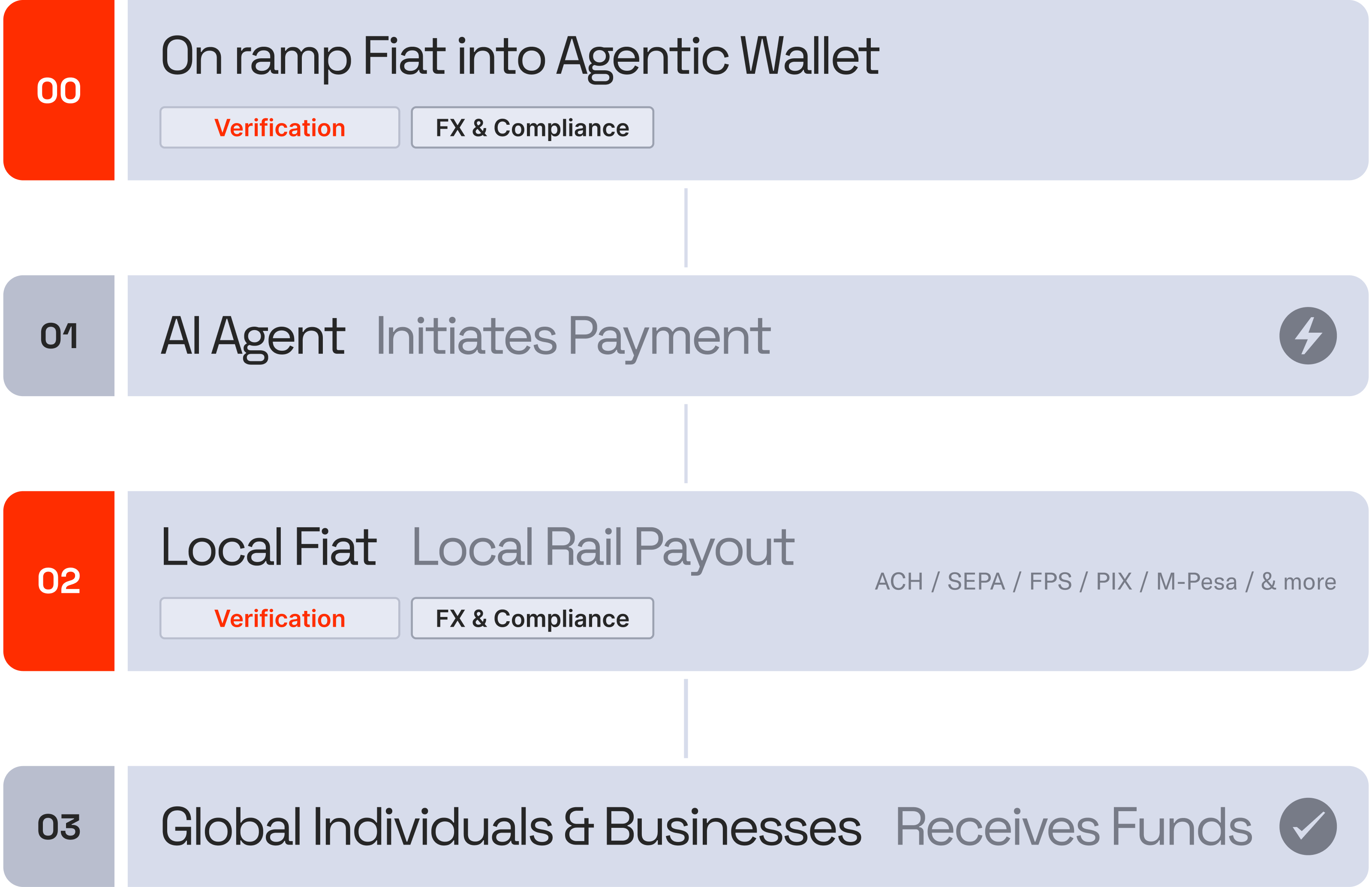

The Last Mile Problem: Why Settlement is the Real Bottleneck

While every protocol currently solves how an agent initiates a payment, settlement remains the real bottleneck. None of the major protocols solve the final, physical step: taking a stablecoin, converting it to local fiat, and delivering it through local rails.

This last mile is incredibly difficult to build because it requires navigating fragmented local payment rails - such as PIX in Brazil or M-Pesa in Kenya - managing real-time foreign exchange, handling per-jurisdiction compliance, and holding regulated entity licensing. For an enterprise, the winning move in agentic commerce is not just building a smart checkout experience; it requires compliance-aware decisioning and regulated B2B2X money movement.

Whoever builds this invisible settlement layer will capture outsized value, operating much like Adyen did for the early internet. This is exactly where infrastructure providers like Noah step in to bridge the gap, serving as the global distribution layer. By sitting beneath the AI protocols, Noah handles what the agent cannot - the FX conversion, the compliance checks, and the local rail delivery.

The resulting transaction flow is highly secure and seamless: an AI agent initiates a payment via a protocol, the payment settles in stablecoins on-chain, and Noah catches that value to convert and route it into local fiat for the recipient. It is entirely invisible to the agent, yet entirely essential to the transaction. The ideal transaction flow moves from the AI Agent → Protocol → Stablecoin → Noah (Settlement) → Local Fiat → Recipient .

What Needs to Happen Next

To truly understand the scale of what is coming, we simply have to look at the path ahead. Currently, data shows that AI agents have executed roughly 140 million payments totaling $43 million over a recent nine-month period. While impressive, this is a drop in the ocean compared to the $3 trillion to $5 trillion that McKinsey projects agentic commerce will orchestrate globally by 2030.

For this multi-trillion-dollar economy to fully materialize, four prerequisites must be met: trust infrastructure must mature, regulatory clarity must be achieved, settlement layers must scale globally, and B2B workflows must lead the way over B2C adoption.

We are currently in a critical 12- to 18-month window. The infrastructure decisions made in 2026 will compound significantly as transaction volumes grow from 2027 through 2030.

Everyone is watching the agents. The real play is in the pipes.